You wear the uniform. You move when the orders say move. You deploy on a week’s notice. And when you return, you open an auto insurance bill that feels like a penalty for your service. Military families face a unique insurance paradox. They deserve the best rates in the country, yet many are overpaying by $400, $600, or more simply because they defaulted to the wrong carrier. Two names dominate the conversation: USAA and GEICO. One was built exclusively for you. The other offers a military discount that can, in very specific scenarios, beat USAA at its own game. Picking wrong because of brand loyalty or a single commercial costs real money. This guide strips away the slogans and gives you the data, the eligibility rules, and the exact scenarios where each carrier wins.

Quick Answer: For active duty, veterans, and their immediate families who qualify, USAA is almost always the cheapest and highest-rated option, with average full-coverage premiums of $1,250–$1,600 per year. GEICO, with its 15% military discount, averages $1,450–$1,750 for the same driver and occasionally beats USAA for drivers under 25, certain high-risk profiles, or those who need a local agent. If you are eligible for USAA, start there. If you are not, or if you are a young enlisted driver, GEICO becomes the strongest alternative in the military space.

We break down the real rate comparisons by state, the deployment protections that matter, the discount stacking math, and the eligibility nuances that most guides ignore.

The USAA Advantage: More Than Just a Discount

USAA is not a discount program layered on top of a civilian insurer. It is a reciprocal exchange owned by its members—military officers, enlisted personnel, veterans, and their families. This structural difference explains why its rates undercut the industry average by 20–25% year after year. USAA does not answer to Wall Street shareholders. It answers to you. The result is a combination of price, service, and military-specific features that no general-market carrier has ever replicated.

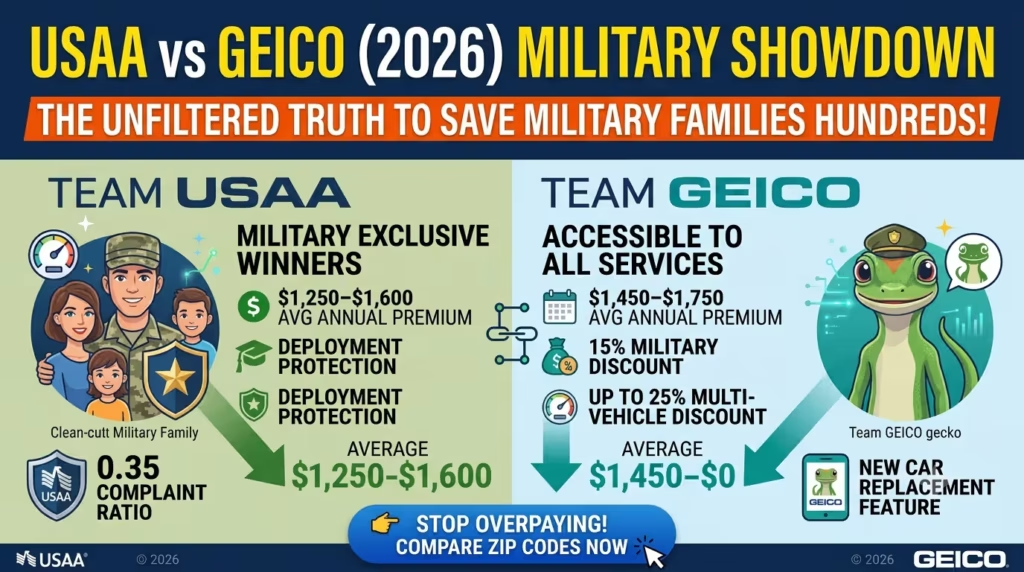

- Average annual premium (full coverage, clean record): $1,250–$1,600 nationally, depending on state and vehicle.

- Deployment protection: You can suspend your coverage while deployed overseas and reinstate it upon return without a lapse penalty. This alone saves hundreds for service members on extended rotations.

- Military installation discount: USAA applies an automatic discount if your vehicle is garaged on a military base.

- Accident forgiveness: Available after five years of claim-free membership, shielding your rate after your first at-fault incident.

- Worldwide claims service: Whether you are stationed in Germany, Japan, or Texas, USAA’s claims infrastructure is built for a mobile military lifestyle.

The NAIC complaint index for USAA sits at an extraordinary 0.35—meaning it receives 65% fewer complaints than expected for an insurer its size. No other major auto insurer comes close. If you qualify, the math is not complicated.

GEICO’s Military Play: Where It Wins and Why

GEICO is not a military-exclusive insurer, but its history is deeply tied to the armed forces. The company was founded to serve government employees and military personnel, and its 15% military discount remains one of the most accessible in the industry. Unlike USAA, GEICO imposes no eligibility restrictions—any active duty, reserve, National Guard, veteran, or retired service member qualifies. This broad access makes GEICO the de facto choice for thousands of military families who fall outside USAA’s stricter eligibility lines.

- Average annual premium (full coverage, clean record, with military discount): $1,450–$1,750 nationally.

- Federal employee discount: If you are a civilian DoD employee or a military spouse working for the federal government, GEICO stacks an additional 12% discount on top of the military discount.

- Local agent access: GEICO maintains a network of local agents in addition to its direct-to-consumer model. USAA operates almost entirely through phone and digital channels.

- Young driver rates: For drivers under 25, GEICO’s pricing model can undercut USAA by $100–$300 annually, especially when the young driver is on their own policy and not a dependent on a parent’s USAA account.

GEICO’s 25% multi-vehicle discount also creates a pricing advantage for military families with three or more cars. If USAA’s multi-vehicle discount caps at a lower percentage in your state, GEICO can win the household total premium battle even if USAA wins the per-vehicle rate.

State-by-State Premium Showdown (2026 Data)

National averages are useful, but your PCS location or home of record dictates your actual bill. Using filed 2026 rates for a 40-year-old driver with a clean record, full coverage (100/300/100 liability, comprehensive and collision with a $500 deductible), and 12,000 annual miles, here is the head-to-head comparison in five major military-populated states:

- Florida: USAA $1,700 vs. GEICO $1,850 — USAA saves $150

- Texas: USAA $1,450 vs. GEICO $1,650 — USAA saves $200

- California: USAA $1,500 vs. GEICO $1,700 — USAA saves $200

- New York: USAA $1,800 vs. GEICO $2,000 — USAA saves $200

- Illinois: USAA $1,150 vs. GEICO $1,300 — USAA saves $150

USAA holds a consistent $150–$200 annual advantage across these states for the standard driver profile. The gap narrows for drivers under 25 and widens again for drivers over 50 with clean records. Always run both quotes using your exact ZIP code and vehicle, because GEICO’s pricing algorithm occasionally produces a lower number in specific rating territories.

Eligibility Deep Dive: Who Actually Qualifies for USAA

The single biggest mistake military families make is assuming they do not qualify for USAA. Eligibility has expanded significantly over the past decade. Here is the definitive list:

- Active duty officers and enlisted personnel across all branches—Army, Navy, Air Force, Marine Corps, Coast Guard, and Space Force.

- Veterans who have retired or separated with an honorable discharge.

- Spouses of USAA members, including surviving spouses who have not remarried.

- Children of USAA members, who can inherit eligibility and pass it to their own children.

- National Guard and Reserve members on active duty for 30 or more days (eligibility may depend on activation status—verify with USAA directly).

If you fall outside these categories, you cannot purchase USAA auto insurance. That is where GEICO becomes your primary target. GEICO does not restrict membership, and its military discount applies broadly without activation requirements.

Deployment and Overseas: The Decisive Factor

Military life is not stationary. One carrier handles the disruption seamlessly. The other requires workarounds. USAA’s deployment suspension feature lets you pause your auto policy while you are deployed to a theater where you are not driving the vehicle. You stop paying premium. You resume coverage when you return with no gap and no penalty. GEICO does not offer a suspension option—you must either maintain the policy, cancel and reapply upon return, or reduce coverage to storage-only comprehensive. Storage coverage is cheaper than full coverage but still costs money, and the lapse in liability coverage can affect your future rates if you cancel entirely. For a six-month Army rotation or a nine-month Navy deployment, USAA’s suspension feature alone can save $400–$800 in unnecessary premium.

If your deployment is imminent, the USAA advantage is categorical. GEICO remains a solid second choice only if you do not qualify for USAA or if your vehicle remains in use by a family member stateside while you are overseas.

Discount Stacking: USAA vs GEICO

Base rates tell half the story. The discounts you stack determine the final number on your declarations page. USAA and GEICO take fundamentally different approaches to discount design.

USAA Discounts (Built for the Military Lifecycle)

- Multi-vehicle discount — varies by state but typically 10–15% per additional car.

- Multi-product discount — add homeowners, renters, or life insurance and your auto rate drops further.

- Good driver discount — clean record for five years triggers a significant reduction.

- Good student discount — full-time students with a B average or better qualify.

- New car discount — vehicles less than three years old often receive a lower base rate.

- Length of membership discount — long-term members receive loyalty-based pricing adjustments.

GEICO Discounts (Broader, With a Telematics Edge)

- Military discount: Up to 15% for active duty, veterans, and retirees.

- Federal employee discount: Up to 12% for civilian government workers, including DoD personnel.

- Multi-vehicle discount: Up to 25%, the highest in the industry.

- Good student discount: Up to 15%.

- Defensive driving discount: 5–10% upon course completion.

- DriveEasy telematics: Up to 20% for safe driving monitored through the GEICO app.

GEICO’s multi-vehicle discount ceiling of 25% can swing a household comparison in its favor if you insure three or more vehicles. USAA’s telematics program exists but is not as aggressively priced as GEICO’s DriveEasy. If you are a low-mileage, safe driver willing to share driving data, GEICO’s telematics discount can close the gap with USAA entirely.

Claims and Customer Satisfaction: The Gap Is Real

Price matters. But the experience after an accident matters more. On this front, the data is unambiguous.

- J.D. Power Overall Satisfaction (2025): USAA consistently scores above 890 out of 1,000, placing it in the highest tier every year. GEICO scores 874, which is above the industry average but not in USAA’s league.

- NAIC Complaint Index: USAA’s complaint ratio is 0.35, the lowest among national carriers. GEICO’s ratio is 0.75, still below the 1.0 baseline but more than double USAA’s.

- Claims speed and transparency: USAA members report faster initial contact, shorter repair times, and fewer disputes over valuations. GEICO’s claims process is efficient but less personal, with heavier reliance on automated workflows.

If you want the highest probability of a frictionless claim, USAA is the statistically superior choice. GEICO is not unreliable—it simply is not in the same tier.

Definitive Buyer’s Guide: Who Chooses Which in 2026

We have distilled the data into actionable profiles. Find your situation and act accordingly.

Choose USAA If…

- You are eligible and want the lowest rate, period.

- You face a deployment or PCS move in the next 12 months and need deployment suspension.

- You value world-class customer satisfaction and claims handling above all else.

- You plan to stay with the same insurer for decades and want membership-based loyalty benefits.

- You also need homeowners, renters, or life insurance and want a single integrated provider.

Choose GEICO (Even If Eligible for USAA) If…

- You are under 25 and USAA’s quote for a young solo policy is unexpectedly high.

- You insure three or more vehicles and GEICO’s 25% multi-vehicle discount delivers a lower household total.

- You want a local agent you can sit down with in person.

- You are a federal civilian employee, and stacking the federal and military discounts beats USAA’s rate.

- You do not qualify for USAA—GEICO’s military discount is the next best thing.

Stop Guessing and Run the Numbers

Military families move more often, deploy without warning, and deserve an insurance company that rewards their sacrifice, not one that exploits their loyalty. Whether you ultimately land with USAA or GEICO, the only error is choosing without comparing. Run both quotes today. Check the deployment provisions. Stack every discount you are entitled to claim. The difference is rarely $50. It is usually $200, $400, or more per year—money that belongs in your pocket, not an insurer’s surplus.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: USAA and GEICO rate filings (2026), Quadrant Information Services, J.D. Power 2025 U.S. Auto Insurance Study, NAIC Complaint Index, company eligibility guidelines and underwriting rules.