After a brutal 46% cumulative surge from 2022 to 2024, car insurance rates in 2026 are finally flashing a different signal — but it’s not the all-clear drivers were hoping for. Nationally, the average premium is projected to inch up by only about 1%, the smallest rise in four years. Yet behind that calm number, your wallet could be hit with a 10% spike or land a 6% discount, depending entirely on your ZIP code and the insurer you choose.

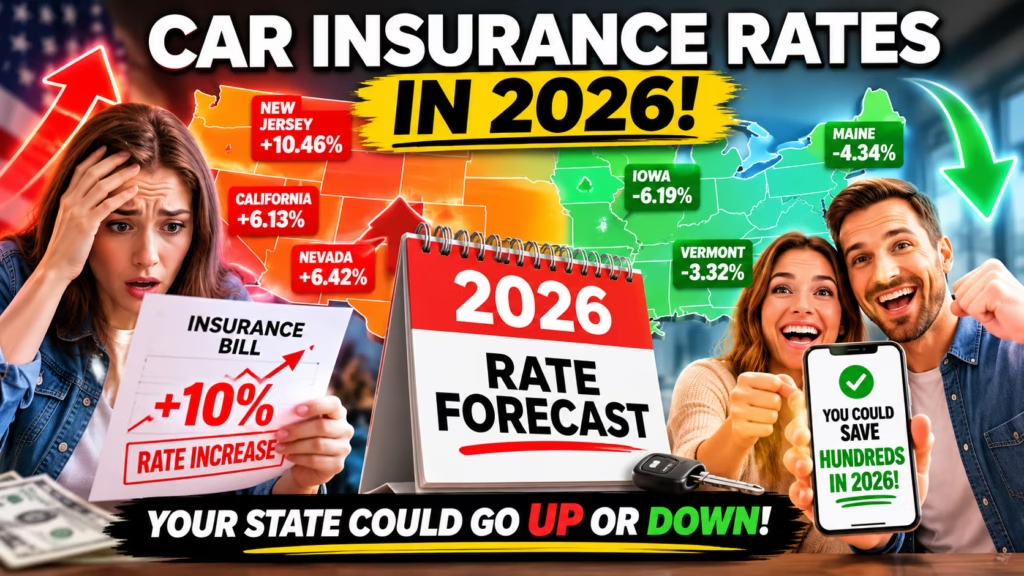

Quick Answer: In 2026, car insurance rates will rise in 35 states but fall in 13. The national average full-coverage premium is projected at $2,158 per year (The Zebra says $2,256). New Jersey drivers face the worst hike (+10.46%), while Iowa drivers could save 6.19%. However, the single most powerful lever is shopping around — price differences between the cheapest and most expensive insurer for the same coverage can hit 406%, slashing monthly bills by over $500.

If you’re reading this, you’re probably wondering: Will my premium go up this year? Is there anything I can do about it? This article gives you the only 2026 forecast that matters — the one for your state and your policy. You’ll see the exact states where rates are climbing, which ones are falling, how major insurers are pricing, and, most importantly, the proven steps to lock in a lower rate before your next renewal hits.

📑 Jump to Section:

The National Picture: A Market in Transition

Let’s put the numbers in perspective. From 2022 through 2024, insurers pushed through massive rate increases to catch up with soaring repair costs, medical claims, and catastrophic weather losses. The result: the average full-coverage premium ballooned from $1,600 to over $2,300. Then, in 2025, the market cooled — the national average actually dropped 6%. For 2026, analysts at ValuePenguin project a mere 1% increase, bringing the average annual premium to $2,158. The Zebra’s model estimates a slightly higher figure of $2,256.

“That’s the smallest year-over-year increase since 2022,” notes ValuePenguin’s latest report. This stabilization signals that the industry is finally restoring underwriting profitability after years of aggressive corrections. But don’t mistake a flat national number for flat bills. The real story is in the state-level disparities — and that’s where your savings opportunity lies.

Get Your Personalized Teen Car Insurance Quote

Enter your ZIP code below to get a highly accurate 2026 estimate based on your exact location, vehicle, and teen driver profile.

Get My ZIP Code Estimate NowStates Where Rates Are Rising the Most

According to The Zebra’s 2026 State of Insurance Report, premiums are projected to increase in 19 states during the first half of the year. ValuePenguin estimates that 35 states will see full-year increases. These aren’t trivial bumps — in some places, you’ll pay hundreds more for the exact same coverage.

Additional states forecast to post significant increases include Oregon (+21%), Maryland (+17%), and Utah (+8%), reflecting regional repair costs and weather risks.

States Where Rates Are Dropping

Not everyone will pay more. 13 states are projected to see rate decreases, offering a welcome reprieve — if you know to shop for it.

Other decliners include Illinois (-4.26%), Indiana, and Nebraska. If you live in one of these states, now is the moment to requote — your current insurer may not have passed the savings on to you yet.

Which Insurance Companies Are Raising or Lowering Rates?

Major insurers aren’t moving in lockstep. In fact, five of the 10 largest auto insurers are expected to lower their rates in 2026. Here’s how the big names stack up:

Remember, these are averages. Your own rate will vary based on your driving record, vehicle, and ZIP code. The critical lesson: loyalty does not pay. A driver switching from a high-cost insurer to the cheapest can slash their premium by $500 per month or more — a 406% price spread, according to recent comparison data.

Why the Mixed Forecast?

Several powerful forces are pulling rates in opposite directions:

- Population shifts and urbanization: Growth in dense, accident-prone areas (Dallas, Atlanta, Phoenix) increases claims frequency, while rural states see fewer losses — creating a widening gap.

- Record shopping activity: A staggering 57% of policyholders shopped for new coverage in the past year. That competitive pressure is forcing insurers to keep rates in check, especially in states with many carrier options.

- Tariffs on parts and vehicles: While tariff impacts on repair costs have not fully materialized, early signs point to higher prices for imported parts and certain electronic components. Insurers are pricing in moderate increases for comprehensive and collision claims.

- Climate and catastrophe losses: Wildfire-prone states (California) and hurricane-exposed regions (Florida) continue to see elevated premiums, while the Midwest benefits from milder loss trends.

- Return to underwriting profitability: After the punishing loss years of 2022-2024, many insurers are now adequately priced. That’s why rate increases are decelerating — but it also means discounts are harder to extract unless you switch carriers.

How to Save Even If Your State Is Going Up

The national trend doesn’t have to be your trend. Use these six hard-hitting tactics to flip the script on rising rates:

- Compare quotes aggressively — don’t auto-renew. The difference between the cheapest and most expensive insurer for identical coverage is as much as $6,000 a year. Spend 15 minutes every six months comparing five quotes; the ROI is enormous.

- Bundle home or renters insurance. This single move often unlocks 10%–20% off both policies. If you don’t have a bundle, get one now.

- Raise your deductible to $1,000. If you have emergency savings to cover it, going from $500 to $1,000 can reduce your premium by 10%–15%. It’s the quickest way to cut cost without losing coverage quality.

- Lock in a 12-month policy. If your state allows annual policies and you find a good rate, grab it. You’ll avoid mid-year increases and often get a small paid-in-full discount.

- Maintain credit above 750. Insurers use credit-based scores in most states. Excellent credit saves you 25%–40% compared to poor credit — that’s $500–$800/year on a full-coverage policy.

- Ask for new-vehicle and good-driver discounts. Even a 2% or 5% reduction stacks up. Mention you’ve taken a defensive driving course (save 5%–10%), sign up for telematics if your driving is safe, and always inquire about loyalty, paperless, and autopay discounts.

Ready to see what your 2026 rate should actually be? Use the free ZIP code estimator below — it pulls real-time data from top insurers and shows you exactly how much you can save in your state.

Get Your Personalized Teen Car Insurance Quote

Enter your ZIP code below to get a highly accurate 2026 estimate based on your exact location, vehicle, and teen driver profile.

Get My ZIP Code Estimate NowFrequently Asked Questions About 2026 Car Insurance Rates

Are car insurance rates going up in 2026?

Nationally, yes — but only by about 1%, the smallest increase since 2022. However, 35 states are projected to see rate increases, with some jumping 10% or more. At the same time, 13 states are expected to record decreases. Your personal outcome depends almost entirely on where you live and which company insures you.

Which states will see the biggest car insurance rate increases in 2026?

New Jersey (+10.46%), Nevada (+6.42%), California (+6.13%), New York (+6.02%), and Washington, D.C. (+5.36%) lead the list. Oregon, Maryland, and Utah are also forecast for 8%–21% hikes due to repair costs, litigation, and population density.

Which states will see the biggest decreases?

Iowa (-6.19%), Minnesota (-5.29%), Arkansas (-4.70%), Missouri (-4.45%), and Illinois (-4.26%) top the decline list. Drivers in these states can still save more by comparing quotes, as not all insurers will pass the savings on automatically.

Is it a good time to switch car insurance companies?

Absolutely. With record shopping activity, insurers are competing aggressively. Five of the top 10 carriers are lowering rates. Comparing quotes now could lock in a 12-month policy at a lower rate before your state’s market shifts again. The spread between the cheapest and most expensive insurer remains extreme — up to 406% — so switching can save hundreds per month.

How can I save on car insurance in 2026?

Start by comparing quotes from at least 5 insurers. Then bundle home/renters, raise your deductible to $1,000, maintain excellent credit, ask about new-car and defensive driving discounts, and pay annually to avoid monthly fees. These steps can easily save 25% or more, even in states with rising average rates.

Bottom Line: Your Rate Isn’t Set in Stone

The 2026 car insurance market is a tale of two countries — a flat national average hiding wild state-level volatility. But your premium isn’t determined by a headline number; it’s determined by your actions. Drivers who shop around, stack discounts, and refuse to auto-renew consistently beat the averages.

Here’s your 3-step action plan right now:

- Check your state’s trend in the lists above. Know whether you’re in a rising or falling market — it sets your baseline expectation.

- Get real quotes from at least 5 insurers using the ZIP code tool below. Don’t rely on advertised rates; they rarely match your profile.

- Implement at least three of the savings tactics — bundle, raise your deductible, and pay annually are the fastest wins.

In a market this uneven, the biggest risk isn’t a rate increase — it’s staying with the same insurer without checking alternatives. Take 30 seconds now to see what your actual 2026 premium should be.

Sources: ValuePenguin 2026 Auto Insurance Rate Forecast, The Zebra State of Insurance Report 2026, Insurify 2026 Rate Analysis, LexisNexis Risk Solutions Auto Insurance Trends Report, Quadrant Information Services, National Association of Insurance Commissioners (NAIC).