Moving between Florida and California triggers a radical shift in your car insurance obligations, rates, and legal protections. In 2026, with insurance premiums surging nationwide due to inflation, weather catastrophes, and litigation costs, the state you call home has never mattered more. One state runs on a strict no-fault system where you can legally drive without bodily injury coverage. The other bans insurers from using your credit score entirely. Getting this wrong when you relocate can mean denied claims, license suspension, or paying thousands more than necessary.

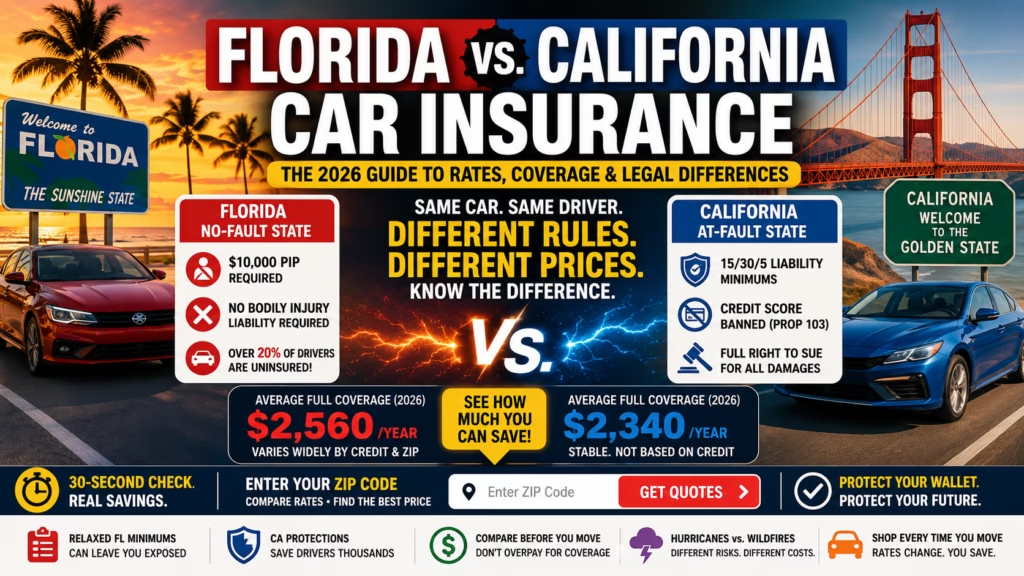

Quick Answer: Florida is a no-fault state requiring Personal Injury Protection (PIP) but — shockingly — no bodily injury liability. California is an at-fault state that completely bans credit-based pricing under Prop 103 and requires 15/30/5 liability minimums. If you have poor credit, California will almost always be cheaper. If you have excellent credit, Florida becomes more competitive, but you must carry Uninsured Motorist coverage because over 20% of Florida drivers have no insurance at all.

This is the only side-by-side breakdown you need to understand the fault systems, coverage gaps, pricing secrets, and the exact steps to switch your policy without a lapse. Here is what every driver relocating between these high-cost states must know in 2026.

At-a-Glance: Florida vs. California Insurance Matrix (2026)

| Coverage Feature | Florida | California |

|---|---|---|

| Fault System | No-Fault — PIP pays your bills first, regardless of fault. Lawsuits restricted to serious injury threshold. | At-Fault (Tort) — The driver who caused the crash pays. Full right to sue for all damages. |

| Minimum Required Coverage | $10,000 PIP + $10,000 Property Damage Liability (PDL). No bodily injury liability required. | 15/30/5 — $15k bodily injury per person, $30k per accident, $5k property damage. |

| Credit Score Impact | Insurers can and do use credit-based insurance scores. Poor credit = significantly higher premiums. | Banned entirely since 1989 (Prop 103). Credit score has zero impact on your rate. |

| Uninsured Motorist (UM) Status | Not required, but insurers must offer it. Over 20% of drivers uninsured — UM is critical. | Not required, but must be offered. Approximately 16.6% uninsured. |

| Rate Regulation | File-and-use — insurers implement rates then file with state. Faster increases. | Prior approval (Prop 103) — Commissioner must approve rate changes before they take effect. |

| Average Full Coverage Premium (2026) | $2,560/year (varies widely by credit and ZIP). | $2,340/year (stable regardless of credit). |

| DUI Consequence | FR-44 — High-risk filing with $100k/$300k liability limits. Extremely expensive. | SR-22 — Standard filing with minimum 15/30/5 limits. |

Florida’s No-Fault Trap: What New Residents Always Miss

Florida belongs to an exclusive club of just 12 no-fault states, and its rules catch transplants off guard every single day. Here is what actually happens after a crash in the Sunshine State:

- Your own PIP coverage pays your medical bills first — regardless of who ran the red light. The minimum is only $10,000, which covers almost nothing in a serious ER visit.

- You cannot sue the at-fault driver unless your injury crosses Florida’s “serious injury” threshold — defined as death, permanent injury, significant disfigurement, or permanent loss of a bodily function. A broken arm that heals perfectly? You likely cannot sue.

- Florida does not legally require bodily injury liability insurance. This is the most dangerous loophole in American auto insurance. A driver can legally carry just $10,000 PIP and $10,000 property damage. If they total your $45,000 SUV and put you in the hospital, their policy pays only $10,000 toward your vehicle and nothing toward your medical bills beyond what your own PIP covers.

This legal vacuum is why Florida consistently ranks among the top states for uninsured drivers (over 20%) and why insurance litigation explodes there. If you move to Florida, you must protect yourself — the other driver’s coverage likely will not.

California’s At-Fault Reality: Higher Stakes, Smarter Protections

California operates under a traditional tort system. The driver who causes the accident pays. This sounds straightforward, but the financial implications run deep:

- Full right to sue — You can recover economic damages (medical bills, lost wages, repair costs) and non-economic damages (pain and suffering, emotional distress) from the at-fault driver’s insurer.

- Minimum limits are dangerously low — 15/30/5 was set decades ago and has not kept pace with inflation. In 2026, a single day in a California ER can exceed $15,000. If the at-fault driver carries only minimum coverage, you may exhaust their policy limits before your hospital discharge papers are signed.

- Prop 103 is California’s consumer shield — Passed in 1988, this law requires the Insurance Commissioner to approve every rate change before it hits your bill. It also permanently banned credit-based insurance scoring, making California one of only three states (alongside Hawaii and Massachusetts) where your FICO score has zero impact on your premium.

The trade-off? Because rate increases require regulatory approval, insurers sometimes exit the California market rather than operate at a loss. This reduced competition can push prices up for everyone. Yet for drivers with damaged credit, California remains a sanctuary compared to Florida.

The Credit Score Divide: Where You Save Thousands

This is the single largest pricing variable between these two states. Florida insurers rely heavily on credit-based insurance scores — a statistical model that correlates credit history with claim likelihood. California insurers cannot touch it.

Here is the real-world premium comparison for a 40-year-old driver with a clean record, 100/300/100 full coverage, and a $500 deductible in 2026:

- Florida — Excellent credit (750+): ~$2,300/year

- Florida — Poor credit (550-600): ~$3,500/year (a 52% surcharge)

- California — Any credit score: ~$2,350/year (flat, no credit adjustment)

If your credit score is below 650, California will almost certainly save you $1,000 or more annually. If your credit is pristine, Florida can be marginally competitive — but you must still factor in the cost of adding Uninsured Motorist and Bodily Injury coverage that Florida’s minimums ignore.

Relocating? Here Is Your Exact Coverage Checklist

Moving from Florida to California

- Drop PIP: California does not recognize Florida’s no-fault coverage. Your PIP becomes worthless the day you register in CA.

- Upgrade liability to at least 100/300/50: California’s 15/30/5 minimums are inadequate. Medical costs and vehicle values demand higher limits. Many agents recommend 100/300/100.

- Expect a rate decrease if your credit is poor: California’s credit ban immediately removes that penalty. You may save significantly.

- Notify your insurer within 30 days: Failing to update your garaging address is considered misrepresentation. Claims can be denied retroactively.

Moving from California to Florida

- Add PIP immediately: $10,000 minimum, but consider higher PIP limits if available — $10,000 disappears fast in a trauma center.

- Add Bodily Injury Liability voluntarily: Florida does not require it, but driving without it is financial suicide. Carry at least 100/300.

- Add Uninsured Motorist coverage (UM): With 1 in 5 Florida drivers uninsured, skipping UM is gambling with your recovery. Match your UM limits to your liability limits.

- Brace for a rate increase if you had good credit in California: Florida’s credit-based pricing will introduce a factor you never faced before.

Special Rules: DUIs, Rideshare, and Weather Risks

DUI Penalties: FR-44 vs. SR-22

Florida’s FR-44 filing for DUI convictions is uniquely punishing. It mandates liability limits of $100,000 per person and $300,000 per accident — nearly seven times higher than California’s SR-22 requirement of 15/30. A Florida DUI can triple your premium overnight and the FR-44 must be maintained for three years. California’s SR-22, while still expensive, operates at standard minimum limits.

Comprehensive Claims: Hurricane vs. Wildfire

Both states face severe weather, but the claim type differs. Florida’s coastal drivers file comprehensive claims for hurricane flood damage and wind-borne debris. This inflates comprehensive premiums in ZIP codes near the Gulf and Atlantic coasts. California drivers face wildfire risk in the wildland-urban interface (WUI), and insurers in certain ZIP codes now require defensive space inspections or risk non-renewal. Both states are seeing insurers pull back from high-risk areas, making it harder to find affordable comprehensive coverage.

Rideshare (TNC) Insurance

Both states mandate rideshare endorsements for Uber and Lyft drivers. California’s Prop 22 created additional coverage requirements during Period 2 (app on, waiting for a ride request) and Period 3 (en route to pick up a passenger). Florida’s rules are less prescriptive but most major insurers offer TNC endorsements that plug the coverage gap. If you drive for a platform in either state, notify your insurer — standard personal auto policies exclude business use.

Top Insurers in Each State (2026 Market Share)

Florida’s competitive landscape: GEICO leads with approximately 23% market share, followed by Progressive (18%) and State Farm (15%). Regional carriers like Tower Hill and Security First specialize in Florida’s unique property risks but may restrict coverage in coastal counties. USAA dominates among military families.

California’s top players: State Farm holds roughly 20% market share, with GEICO (15%) and Progressive (12%) behind. Mercury Insurance — a California-founded carrier — often delivers the most competitive rates for clean-record drivers. AAA (Automobile Club of Southern California) excels at bundling home and auto policies.

The key takeaway: loyalty to one insurer across state lines rarely pays. A company that dominated in Florida may be overpriced in California. Always re-shop your policy when you move.

Frequently Asked Questions

Is it true Florida drivers can legally drive without bodily injury insurance?

Yes. Florida only requires $10,000 in PIP and $10,000 in property damage liability. There is no mandatory bodily injury liability coverage. This is legal but extraordinarily risky — if you cause an accident, the injured party can sue you personally for medical costs, lost wages, and pain and suffering. Your wages can be garnished and assets seized. Always carry voluntary BI coverage in Florida.

Why did my premium drop after moving from Florida to California with bad credit?

California’s Proposition 103 (1988) prohibits insurers from using credit scores, credit history, or credit-based insurance scores in underwriting or rating. If you had poor credit in Florida, that surcharge disappeared the moment you registered your vehicle in California. This is a permanent consumer protection, not a temporary discount.

Can I keep my Florida PIP policy if I move to California temporarily?

No. Insurance policies are state-specific contracts. If you establish residency in California (register to vote, get a CA driver’s license, or register your vehicle), you must carry a California-compliant policy. A Florida PIP policy provides no valid coverage in an at-fault state. Any gap between your old and new policy is a lapse that will increase your future premiums.

Which state penalizes DUIs more severely on insurance?

Florida, without question. The FR-44 filing requires $100k/$300k liability limits — far above the standard minimum — and insurers price that risk aggressively. A first-time DUI in Florida can push annual premiums above $5,000. California’s SR-22 operates at lower limits, though rates still spike sharply after any DUI conviction.

The Bottom Line: Protect Yourself by Shopping Smart

Florida and California represent opposite ends of the American auto insurance spectrum. Florida’s no-fault experiment leaves drivers dangerously underinsured unless they proactively add coverage the state does not mandate. California’s regulatory framework shields consumers from credit discrimination but cannot fully tame the cost of living in the most populous state.

No matter which state you call home — or if you are standing at the border trying to decide — the only way to know your true rate is to compare quotes from multiple insurers in your specific ZIP code. A 30-second check today can reveal whether you are overpaying by hundreds or even thousands of dollars annually. Enter your ZIP code below to compare baseline rates and see exactly how much your coverage should cost in 2026.

Sources: Florida Office of Insurance Regulation (FLOIR) 2026 Auto Insurance Data Call, California Department of Insurance (CDI) Rate Comparison Survey, Insurance Information Institute (III) No-Fault State Fact Sheet, National Association of Insurance Commissioners (NAIC) Auto Insurance Database Report, Quadrant Information Services Premium Analytics, California Proposition 103 (Insurance Rate Reduction and Reform Act of 1988).

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.