Your teenager passed the driving test. You breathed a sigh of relief—until your insurance agent gave you the updated premium. Adding a 16- or 17-year-old to a family policy in 2026 spikes your annual bill by 80% to 150%, often adding $1,500 to $4,000 per year. Parents across the country are making the same expensive mistake: they add the teen to their current policy without shopping around first. The insurance company that gave you the best rate as a married adult couple is rarely the cheapest when a newly licensed operator enters the household. The carriers that win for teen drivers are those with the deepest good-student discounts, telematics programs that reward safe driving, and regional specialists who price young risk better than the national giants. This state-by-state guide hands you the exact companies, discounts, and strategies to cut that jaw-dropping premium in half.

Quick Answer: The cheapest way to insure a teen driver is to add them to your existing family policy and aggressively stack every discount available—good student (up to 25%), defensive driving course, and telematics monitoring. Nationally, GEICO, USAA (military), and regional carriers like Erie and Westfield offer the most competitive teen rates, with total annual family premiums ranging from $1,700 to $4,500 depending on your state, the car they drive, and the discounts you claim.

We break down the real cost of insuring a teen driver in 2026, the discounts that actually move the needle, and the best insurance companies by state so you can stop overpaying before the next bill arrives.

The True Cost of Adding a Teen Driver in 2026

Carriers price young drivers based on cold, hard actuarial data. Drivers aged 16–19 are involved in fatal crashes at nearly three times the rate of drivers aged 20 and older, according to NHTSA. This risk translates directly into premium hikes. Adding a single teen to a two-car, full-coverage family policy typically increases the annual bill by $1,500 to $4,000, depending on your state and whether the teen drives a car of their own or shares a family vehicle. A separate policy for a teen is almost never the answer—it can cost two to three times more than being rated on a parent’s multi-vehicle policy. The key to affordability lies entirely in which carrier you choose and how many discounts you stack.

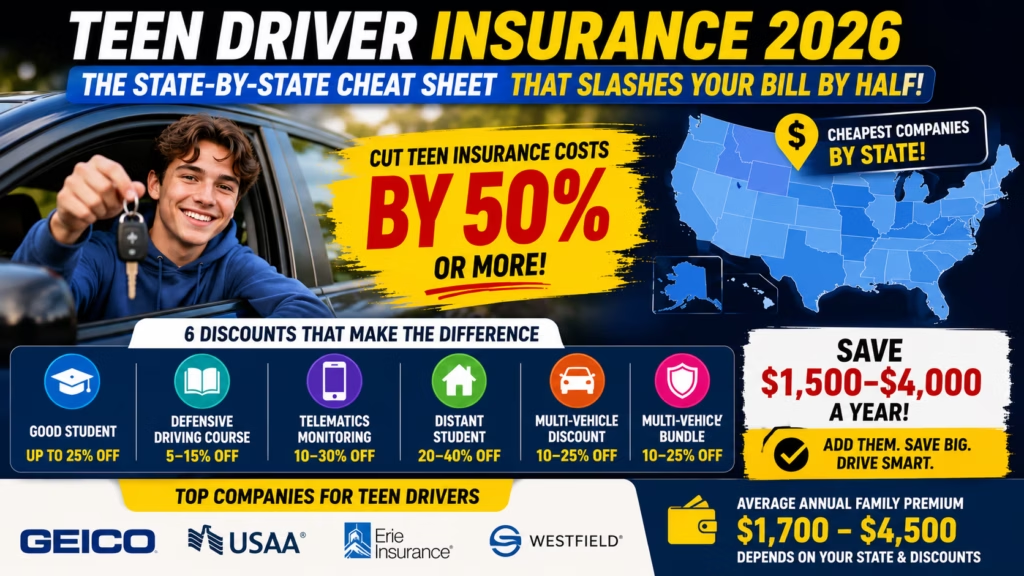

6 Discounts That Can Slash Teen Premiums by 50%

Before you look at a single quote, know which discounts to demand. These six can turn a $4,000 annual bill into $2,000 or less.

- Good Student Discount: Maintaining a B average or a 3.0 GPA unlocks savings of 10–25% with nearly every major carrier. This is the single most powerful discount for a teen driver.

- Defensive Driving Course: Many states require or strongly incentivize a state-approved course. Completion earns a 5–15% discount that typically lasts three years.

- Telematics or Monitoring App: Programs like Progressive’s Snapshot, State Farm’s Drive Safe & Save, and GEICO’s DriveEasy track real-world driving. Teens who avoid hard braking, late-night driving, and excessive speed can earn discounts of 10–30%.

- Distant Student Discount: If your child attends college more than 100 miles away and does not take a car, you can remove them as a primary operator and slash the premium by 20–40% during the academic year.

- Multi-Vehicle Discount: Adding your teen’s car to an existing multi-car policy often saves 10–25% compared to a standalone policy.

- Multi-Policy Bundle: Combine auto with homeowners or renters insurance for an additional 10–20% off the total household premium.

Best Insurers for Teen Drivers by State (2026 Data)

The cheapest carrier for a teen driver is not universal—it shifts by state regulations, rating territories, and the discounts each company prioritizes. Below we map the top contenders for major states based on average 2026 filed rates for a family with two adults and one teen driver on a full-coverage policy.

Florida

Best companies: USAA ($2,400/year if eligible), GEICO ($2,800), Progressive ($3,100). Florida’s no-fault laws and high uninsured motorist rates inflate all premiums. The good student and distant student discounts are essential, and USAA’s military affiliation offers the deepest savings for qualifying families.

Texas

Best companies: USAA ($2,100), GEICO ($2,300), Progressive ($2,500). Texas mandates a six-month learner’s permit and a state-approved driver education course. Many insurers tie their discount to completion of that course.

California

Best companies: Mercury Insurance ($2,200), GEICO ($2,400), State Farm ($2,600). California’s ban on credit-based pricing helps teens who lack credit history. Driver’s education and behind-the-wheel training are legally required before licensing.

New York

Best companies: GEICO ($3,200), Progressive ($3,500), State Farm ($3,600). High PIP requirements and dense urban traffic drive premiums up. The good student discount and defensive driving courses are non-negotiable for keeping costs manageable.

Illinois

Best companies: USAA ($1,800), GEICO ($1,950), Progressive ($2,100). Illinois requires formal driver’s education for teens under 18. Both State Farm and GEICO offer solid multi-vehicle stacking here.

Pennsylvania

Best companies: Erie Insurance ($2,000), GEICO ($2,100), USAA ($1,900). Erie’s strong regional presence and generous good-student discount make it the carrier to beat. Pennsylvania’s “limited tort” option can also reduce premiums by 10–20%.

Ohio

Best companies: Westfield Insurance ($1,700), GEICO ($1,800), Progressive ($1,900). Ohio’s competitive market and moderate risk profile keep teen premiums lower than the national average. Regional carriers like Westfield and Grange often undercut the nationals by 10–15%.

The Car Your Teen Drives Matters as Much as the Policy

Insurers do not rate all vehicles equally. A 16-year-old driving a late-model sports car will add far more to your premium than the same teen driving a safe, used sedan. The cheapest vehicles to insure for a teen are typically mid-size sedans and small SUVs with high safety ratings, anti-lock brakes, and passive restraint systems. Avoid vehicles with high horsepower, limited crash-test data, or expensive repair costs. A used Honda Accord or Toyota RAV4 will almost always carry a lower premium than a Mustang or a full-size pickup.

How to Build a Teen Policy That Doesn’t Bankrupt You

- Add the teen to your existing family policy. A separate policy for a teenager is the most expensive option in every state.

- Designate them as a secondary driver on the safest car. Insurers rate drivers on specific vehicles. Assign your teen to the cheapest-to-insure car in your household.

- Increase your deductibles. Moving from $500 to $1,000 on collision and comprehensive can save 10–15%.

- Enroll in a telematics program immediately. The first six months of monitoring often produce the biggest discount because the app establishes a safe driving baseline.

- Shop the policy every six months. A carrier that was cheapest for a family of two may be $800 more expensive once a teen is added. Loyalty does not pay.

- Ask about regional carriers. Companies like Erie, Westfield, Auto-Owners, and Mercury do not always appear on national comparison sites but can beat the giants by a wide margin.

Stop Guessing and Start Saving

The addition of a teen driver does not have to mean financial panic. The parents who pay the least are not the ones who accept their renewal notice blindly. They are the ones who run side-by-side quotes from USAA, GEICO, and at least one regional carrier, stack every discount available, and put their teen in a safe vehicle with a telematics app running from day one. In the time it takes to watch a sitcom episode, you can benchmark what your premium should actually be.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: Quadrant Information Services (2026 rate filings), National Highway Traffic Safety Administration (NHTSA), Insurance Information Institute (III), state DMV teen driving requirements, NAIC complaint index.