You are a safe driver living in a state where the average full-coverage premium barely scrapes $1,400. Yet your renewal bill just crossed $1,800. You ask yourself a single question: how is it possible that drivers in Cleveland, Columbus, and Cincinnati are paying $1,050 or less for the same coverage while you overpay by hundreds? Ohio’s auto insurance market is one of the friendliest in the nation—low population density outside the major metros, an at-fault tort system that discourages frivolous litigation, and a fiercely competitive carrier landscape. But friendliness means nothing if you are parked with the wrong company. The cheapest Ohio policies belong to drivers who know which regional carriers to invite into the fight and which national names to walk away from.

Quick Answer: The absolute cheapest car insurance in Ohio for a driver with a clean record is USAA at $1,050/year for military families, followed by GEICO at $1,150/year for the general population. Regional carriers Westfield Insurance ($1,200/year) and Grange Insurance ($1,300/year) also undercut the national average by a wide margin. To lock in these rates, you must carry at least 100/300/100 liability, maintain continuous coverage without lapses, and stack every discount available—multi-policy, good student, and defensive driving course completion.

This guide maps out the cheapest car insurance companies in the Buckeye State using 2026 filed rates, breaks down the city-by-city premium swings, and equips you with the exact money-saving tactics that can drop your annual bill by $400 or more before your next renewal.

Why Ohio Is One of the Cheapest States for Car Insurance

Ohio consistently ranks among the ten least expensive states for auto insurance, and the math behind that ranking is straightforward. Unlike no-fault states that bake medical claim inflation into every policy, Ohio operates under a traditional tort system. The driver who causes the accident pays. This single structural difference suppresses fraudulent medical claims and keeps liability premiums in check. Beyond the legal framework, Ohio benefits from moderate traffic density outside its three largest cities, a competitive insurance marketplace with strong regional players, and winter weather that—while occasionally severe—does not produce the catastrophic hurricane or wildfire losses that plague coastal and western states. The average annual full-coverage premium sits near $1,400, roughly 25% below the national average. But that average conceals a spread of over $600 between the cheapest and most expensive carriers.

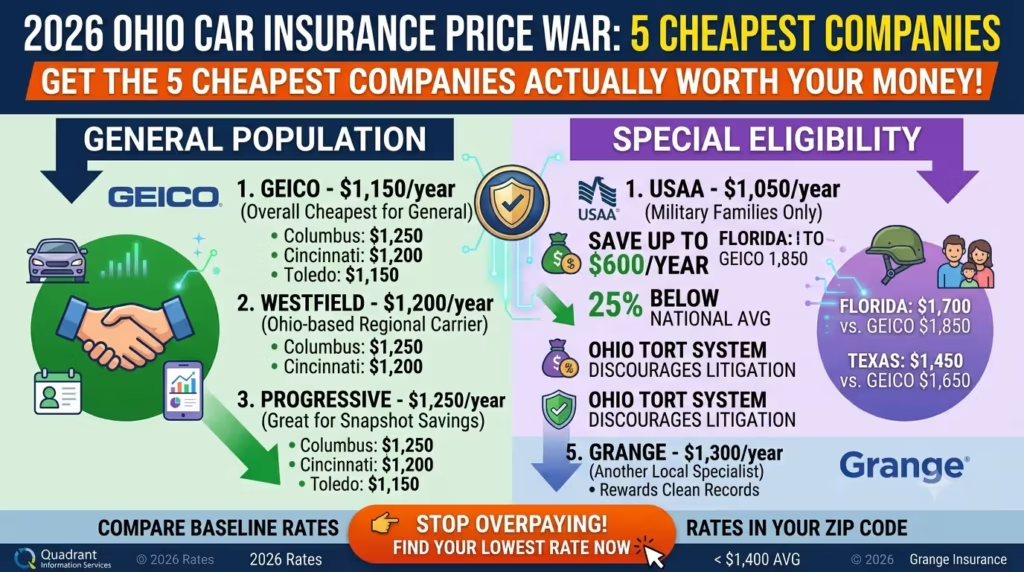

The 5 Cheapest Car Insurance Companies in Ohio (2026 Rate Data)

Using the latest filed rates from Quadrant Information Services for a 40-year-old driver with a clean record, full coverage (100/300/100 liability, comprehensive and collision with a $500 deductible), and 12,000 annual miles, here is the definitive Ohio ranking:

- 1. USAA – $1,050/year (available only to military members, veterans, and their immediate families; if you qualify, this is your stop)

- 2. GEICO – $1,150/year (best overall for the general population; extremely competitive in Columbus, Cincinnati, and Dayton)

- 3. Westfield Insurance – $1,200/year (Ohio-based regional carrier with deep local knowledge and strong bundling discounts for home and auto)

- 4. Progressive – $1,250/year (strong for drivers with one minor violation, young drivers, and anyone willing to enroll in the Snapshot telematics program)

- 5. Grange Insurance – $1,300/year (another Ohio-based regional specialist that rewards clean records and multi-policy households)

State Farm follows closely at $1,350/year and becomes a top-three contender when bundling homeowners or renters coverage. Allstate and Farmers hover in the $1,550–$1,600 range, while non-standard carriers like The General often exceed $1,700 for full coverage. If your driving record is clean and your credit is solid, you should never pay non-standard rates in Ohio.

City-by-City: How Your ZIP Code Shapes Your Ohio Premium

Cleveland is not Springfield. The difference between Ohio’s most expensive and least expensive cities can exceed $400 annually for the identical driver and vehicle. Here are average full-coverage premiums for the cheapest available carrier (GEICO, unless military) across major Ohio metro areas:

- Cleveland: $1,400 (highest in the state due to lake-effect weather, higher traffic density, and elevated claim frequency)

- Columbus: $1,250

- Cincinnati: $1,200

- Akron: $1,180

- Toledo: $1,150

- Dayton: $1,100

- Youngstown: $1,050

- Springfield: $1,000 (lower population density and accident rates push premiums to the state floor)

A 30-mile move can shift your annual premium by 8–12%. Always run quotes using your exact ZIP code—not a metro-area average—because neighborhood-level claim data is baked into every carrier’s pricing algorithm.

Ohio Minimum Coverage Requirements: Don’t Leave Yourself Exposed

Ohio law mandates minimum liability limits of 25/50/25—$25,000 for bodily injury per person, $50,000 per accident, and $25,000 for property damage. These are among the lowest required limits in the country. Carrying only the state minimum will save you $200–$350 a year on premiums and simultaneously expose your personal assets to seizure after any serious at-fault accident. If you injure someone and their medical bills exceed $25,000—a near certainty in any hospitalization scenario—the injured party can pursue your wages, bank accounts, and property for the difference. A responsible Ohio policy starts at 100/300/100 liability limits with matching Uninsured/Underinsured Motorist (UM/UIM) coverage. Ohio insurers must offer UM/UIM, but you can reject it in writing. Rejecting it is a gamble that saves $80–$150 a year and could cost you everything if an uninsured driver runs a red light.

Six Proven Ways to Lower Your Ohio Premium Today

- Bundle your auto with homeowners or renters insurance. State Farm, GEICO, and Westfield deliver the most aggressive multi-policy discounts in Ohio, often shaving 15–20% off your auto premium.

- Complete an Ohio-approved defensive driving course. Even with a spotless record, finishing a short online course ($20–$40) unlocks a 5–10% discount with most carriers, valid for three years.

- Raise your comprehensive and collision deductibles. Moving from $500 to $1,000 reduces your premium by 10–14%. Ohio’s moderate weather risk makes this a smart trade-off for most drivers.

- Enroll in a usage-based telematics program. Progressive’s Snapshot and State Farm’s Drive Safe & Save can deliver 10–30% savings if you drive fewer miles, avoid hard braking, and stay off the roads late at night.

- Pay your premium in full every six or twelve months. Installment fees add $5–$12 per month. Paying upfront eliminates these charges and often triggers an additional paid-in-full discount.

- Request quotes from Ohio-based regional carriers. Westfield, Grange, and Auto-Owners do not always appear on national comparison sites, but their rates beat the nationals by 10–18% for qualifying drivers.

Special Ohio Considerations: Winter, SR-22, and Rideshare

Winter Weather and Comprehensive Coverage

Ohio winters deliver snow, ice, and the occasional pileup. Comprehensive coverage protects against weather-related damage—fallen tree limbs, ice-induced slides into guardrails, and flood damage from spring thaws. Dropping comprehensive to save money is a calculated risk that backfires the moment a winter storm totals your vehicle. Keep the coverage, raise the deductible instead, and make sure your policy does not exclude weather-related claims.

SR-22 and High-Risk Insurance After a Violation

Ohio requires an SR-22 certificate for DUI convictions, driving without insurance, and certain serious moving violations. You must carry the SR-22 for three to five years depending on the offense. Progressive and The General are the most accessible SR-22 carriers in the state. Expect your premium to climb to $2,200–$3,500 annually depending on the severity of the violation and your ZIP code. Once the SR-22 requirement expires, requote immediately—rates drop significantly the moment the filing is removed.

Rideshare and Delivery Driving

If you drive for Uber, Lyft, DoorDash, or Instacart in Ohio, your personal auto policy will not cover you during Periods 1 and 2 (app on waiting for a request, and matched with a rider or order en route). A rideshare endorsement costs $15–$30 per month and closes that coverage gap entirely. State Farm, GEICO, and Progressive all offer rideshare endorsements in Ohio. Driving without one is effectively driving uninsured during every delivery shift.

Stop Overpaying for Ohio Car Insurance Right Now

Ohio’s insurance market rewards shoppers, not loyalists. The carrier that offered you the best rate two years ago may now be $500 more expensive than a competitor you have never heard of. Start with USAA if you have a military connection. Then run side-by-side quotes from GEICO, Westfield, and Progressive. Stack every discount you are entitled to claim. Carry at least 100/300/100 liability limits and never reject uninsured motorist coverage. The Buckeye State gives you every tool to drive your premium well below the national average—if you pick up the phone and use them.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: Ohio Department of Insurance, Quadrant Information Services (2026 rate filings), Insurance Information Institute (III), National Association of Insurance Commissioners (NAIC) complaint index, company underwriting guidelines.