You are standing at a fork in the road. On one side, the familiar red-and-white logo of State Farm, backed by the largest agent network in the country. On the other, the blue-and-white shield of Allstate, promising accident forgiveness and vanishing deductibles. Your decision will lock in an annual premium that could be $1,600 or $2,300 for the exact same coverage. Most drivers pick based on a jingle or a neighbor’s recommendation. That is a $700 mistake. State Farm and Allstate occupy the same heavyweight division, but their pricing algorithms, discount structures, and claims philosophies are radically different. One is built for the cost-conscious family stacking discounts. The other is built for the driver willing to pay a premium for bells and whistles. This comparison tears away the marketing veneer.

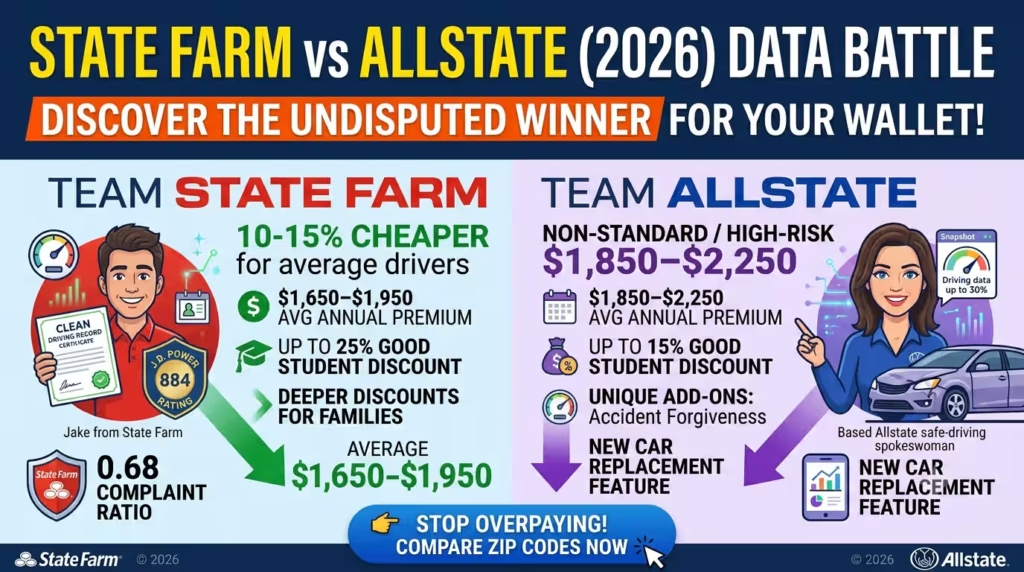

Quick Answer: For the average driver with a clean record, State Farm is 10–15% cheaper than Allstate, with average full-coverage premiums of $1,650–$1,950 compared to Allstate’s $1,850–$2,250. State Farm also wins on customer satisfaction and complaint ratios. Choose Allstate only if you specifically value its unique add-ons—accident forgiveness, vanishing deductible, and new car replacement—and are willing to pay $200–$400 more annually to get them.

We dissect the rate data, discount fine print, bundling strength, and claims experience so you can choose with confidence and keep your money where it belongs.

Head-to-Head Premium Breakdown for 2026

When we analyze aggregated rate filings for a 40-year-old driver with full coverage (100/300/100 liability, comprehensive and collision with a $500 deductible) and 12,000 annual miles, a clear pricing hierarchy emerges. National averages mask state volatility, but the margin between these two carriers is consistent across nearly every region.

- State Farm Average Annual Premium: $1,650–$1,950

- Allstate Average Annual Premium: $1,850–$2,250

State Farm’s pricing advantage stems from its mutual company structure and massive scale, which allows it to operate on thinner margins. Allstate, as a publicly traded company, carries higher acquisition costs and tends to price its base policy higher while offering more optional coverage riders. The gap widens significantly for drivers with teen operators, as State Farm’s good student discount of up to 25% dwarfs Allstate’s 15% cap on the same discount.

Discount Stacking: The Engine That Drives Your Final Price

A base rate without discounts applied is a sticker price nobody should pay. Both companies offer robust discount menus, but the depth and stacking rules differ dramatically.

State Farm Discounts (Deeper and Broader for Families)

State Farm rewards traditional low-risk behaviors and family bundling with discounts that multiply quickly.

- Good Student: Up to 25% for full-time students maintaining a B average or better—the most aggressive student discount in the industry.

- Multi-Vehicle: Up to 20% when you insure two or more cars.

- Good Driver: Up to 15% for drivers with no accidents or violations in the last five years.

- Drive Safe & Save Telematics: Up to 30% savings for safe driving monitored through the mobile app or OnStar.

- Defensive Driving: 5–10% upon completion of a state-approved course.

- Anti-Theft and Vehicle Safety Features: 5–10% each for passive restraints, anti-lock brakes, and alarm systems.

Allstate Discounts (Focused on Payment Behavior and New Cars)

Allstate’s discount structure leans into financial behavior and new-vehicle ownership rather than pure driving merit.

- Drivewise Telematics: Up to 25% for safe driving, though the average realized savings is closer to 15%.

- Good Student: Up to 15% for students with a B average.

- Paid-in-Full: Up to 10% when you pay your entire term upfront.

- E-sign and Auto-Pay: 5–10% combined for paperless billing and automatic payments.

- New Car Discount: Up to 10% for vehicles that are the current model year or one year old.

- Multi-Vehicle: Up to 10%—noticeably less generous than State Farm’s 20% cap.

Verdict: If you are a parent with a teen driver or a household with multiple vehicles, State Farm’s discount architecture will almost certainly deliver a lower final premium. Allstate’s discounts are competitive only if you buy a brand-new car, pay in full, and enroll in Drivewise immediately.

Bundling Power: Home, Renters, and Life Insurance

Both carriers push multi-policy bundling aggressively, but the execution and savings are not equal. State Farm operates a highly integrated system where your auto, home, and life policies sit under one roof with a single agent. The multi-policy discount on auto insurance can reach 17% when bundled with homeowners or renters insurance. Allstate offers competitive bundling as well, typically shaving 10–15% off the auto premium, but its homeowners rates are often higher than State Farm’s, eroding the net savings. If you own a home and insure it with the same carrier, State Farm’s combined auto-plus-home package is the cheaper option in 42 of 50 states based on 2026 filings.

Claims Satisfaction and Customer Service: Where the Gap Widens

Price matters only if the company shows up when you file a claim. Independent data from J.D. Power and the NAIC reveals a clear service gap.

- J.D. Power Overall Satisfaction (2025): State Farm scored 884 out of 1,000, placing it among the top five nationwide. Allstate scored 868, above average but trailing State Farm by a statistically significant margin.

- NAIC Complaint Index: State Farm’s complaint ratio is 0.68, meaning it receives 32% fewer complaints than expected for a company its size. Allstate’s ratio is 0.95, closer to the industry baseline of 1.0 but still higher than State Farm’s.

- Claims Speed: State Farm consistently ranks higher for first-contact speed and settlement turnaround, in part because its captive agent network acts as a local liaison. Allstate’s claims process is fully functional but relies more heavily on call centers and the mobile app.

- Agent Network: State Farm has the largest exclusive-agent network in the United States, with over 19,000 agents. If you prefer a face-to-face relationship, State Farm offers an unmatched local presence. Allstate’s agent network is substantial but smaller, and many policyholders interact primarily through the app.

The data points in one direction: State Farm delivers a higher-loyalty experience. Allstate is not poor—it simply is not as refined in claims handling.

Unique Allstate Features Worth Paying For

Allstate is not without its weapons. If you are willing to pay the premium, certain Allstate-exclusive features hold genuine value.

- Accident Forgiveness: Available as an add-on or earned after a period of clean driving. Your first at-fault accident does not raise your rates. State Farm offers accident forgiveness in limited states, but it is not a core part of its value proposition.

- Vanishing Deductible: Your collision deductible shrinks by $100 for every year you drive without an accident, eventually reaching zero in some configurations. This rewards long-term safe drivers with a tangible benefit.

- New Car Replacement: If your new car is totaled within the first two model years, Allstate pays to replace it with a brand-new vehicle of the same make and model, not just the depreciated actual cash value. This alone can justify the premium for a driver with a $40,000 vehicle.

These features have no direct equivalent at State Farm. If you prioritize them, Allstate is the logical choice, but you must calculate whether the $300–$500 annual premium difference is worth a vanishing deductible that may take five years to matter.

Definitive Buyer’s Guide: Who Chooses Which in 2026

We have consolidated the data into clear profiles. Match your situation to the carrier that fits.

Choose State Farm If…

- You want the lowest possible rate for identical coverage limits.

- You have a teen driver in the household (the 25% good student discount is unbeatable).

- You bundle auto with homeowners, renters, or life insurance.

- You prefer a local agent you can visit in person.

- You value a proven, low-complaint claims experience above all else.

Choose Allstate If…

- You drive a brand-new vehicle and want guaranteed new car replacement.

- You are willing to pay more for accident forgiveness and a vanishing deductible.

- You prefer managing your policy entirely through a highly rated mobile app.

- You have a clean record and can qualify for the full Drivewise discount to narrow the rate gap.

The 10-Minute Rule That Pays Off Immediately

Both State Farm and Allstate let you bind a quote online or through a local agent in under ten minutes. The only wrong move is choosing based on brand recognition instead of running actual numbers for your ZIP code, vehicle, and household composition. State Farm wins on price and service for most drivers. Allstate wins on premium features for those who want them. Your job is to get both quotes, compare the line items, and refuse to pay one cent more than the math requires.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: State Farm and Allstate rate filings (2026), Quadrant Information Services, J.D. Power 2025 U.S. Auto Insurance Study, NAIC Complaint Index, company underwriting guidelines.