You are staring at two quotes separated by a few hundred dollars. On the left, GEICO. On the right, Progressive. Both are industry giants, both have funny commercials, and both want your business. But here is the trap most drivers fall into: they pick based on a single premium number without reverse-engineering what they are actually buying. GEICO typically rewards the low-risk, credit-strong, military-connected driver. Progressive often bends over backwards for the person with a speeding ticket, a lapse in coverage, or a teenager on the policy. Choosing wrong costs you $400, $600, or $1,000 a year in unnecessary premium.

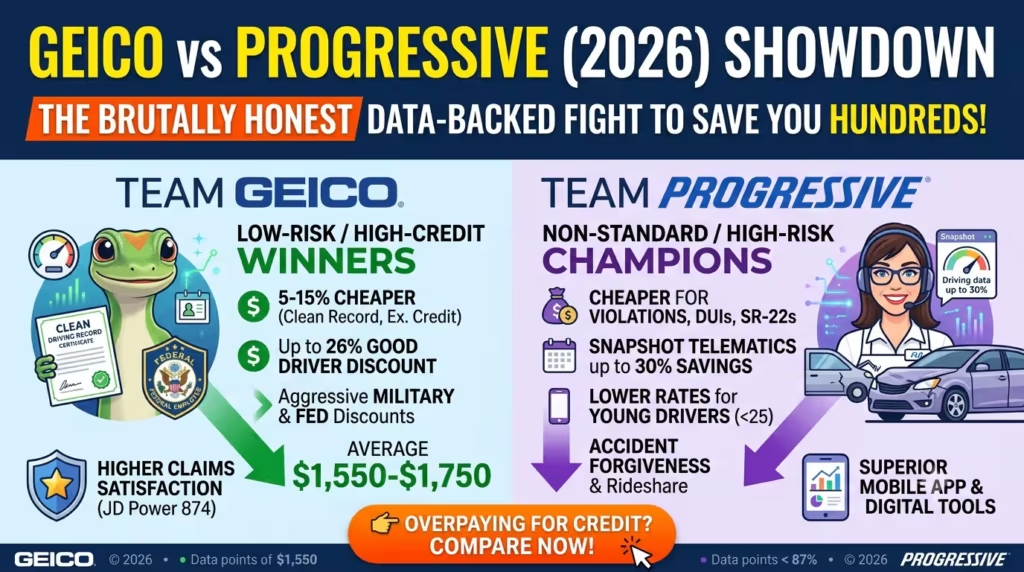

Quick Answer: For a driver with a clean record and excellent credit, GEICO is 5–15% cheaper, averaging $1,550–$1,750 annually for full coverage. If you have a violation, poor credit, or an SR-22 requirement, Progressive is often the cheaper choice, especially when you stack the Snapshot telematics discount. The critical split is your risk profile: low-risk drivers win with GEICO; non-standard and high-risk drivers win with Progressive.

This comparison strips away the marketing fluff. We break down exact rate spreads, discount fine print, claims satisfaction data, and the specific driver profiles that tip the scale in favor of one carrier over the other.

Head-to-Head Premium Analysis for 2026

Using aggregated rate filings for a 40-year-old driver carrying full coverage (100/300/100 liability, comprehensive and collision with a $500 deductible) and driving 12,000 miles annually, the price gap becomes immediately visible. National averages smooth out state-specific volatility, but the delta is consistent across most regions.

- GEICO Average Annual Premium: $1,550–$1,750

- Progressive Average Annual Premium: $1,650–$1,950

GEICO maintains a structural pricing advantage for clean, preferred risks because its underwriting model aggressively pursues low-loss-ratio business. Progressive, on the other hand, prices competitively across a broader risk spectrum, which slightly elevates its baseline for tier-one drivers but dramatically lowers it for tier-three drivers. If your credit score is above 700 and your motor vehicle record is empty, GEICO almost always wins by a margin of 8–12%.

Discount Stacking: The Real Decider of Your Final Bill

Comparing base rates without factoring in discount stacking is like comparing airfare without baggage fees. GEICO and Progressive take fundamentally different approaches to how they shave dollars off your premium.

GEICO Discounts (Aggressive for Affinity Groups)

GEICO leans heavily into affinity and occupational discounts. If you check multiple boxes here, the savings compound quickly.

- Multi-Vehicle: Up to 25%—one of the most aggressive in the industry.

- Good Driver (5 Years Clean): Up to 26% for drivers with no accidents or violations.

- Military: Up to 15% for active duty, veterans, and retired military.

- Federal Employee: Up to 12%—a unique discount that covers civilian government workers.

- Good Student: Up to 15% for full-time students with a B average or better.

- Defensive Driving Course: 5–10% upon completion of a state-approved course.

Progressive Discounts (Aggressive for Telematics and Loyalty)

Progressive counterbalances its slightly higher base rates with a telematics program that can swing a policy from expensive to cheapest-in-class for the right driver.

- Snapshot Telematics: Up to 30% average savings for safe drivers who avoid hard braking, late-night driving, and excessive mileage.

- Paid-in-Full: Up to 10% when you pay your entire six- or twelve-month term upfront.

- Multi-Vehicle: Up to 12% for insuring more than one car.

- Continuous Insurance: 5–10% if you have maintained coverage without a lapse.

- Homeowner Discount: 5–10% whether you own a house, condo, or townhome.

- Good Student: Up to 10% for students maintaining a B average.

Verdict: If you are a federal employee or military member with a multi-car household, GEICO’s affinity discounts create a moat that Progressive cannot cross. If you are a low-mileage, safe driver willing to let an app monitor your habits for six months, Progressive’s Snapshot can produce the single largest discount available between the two companies.

High-Risk Drivers: Where Progressive Pulls Ahead

The moment a violation, accident, or DUI enters your driving record, the pricing equation flips. GEICO’s underwriting appetite narrows significantly for non-standard risks, while Progressive built its brand on insuring the drivers other carriers reject.

- One At-Fault Accident: GEICO’s premium spikes 45–65% on renewal. Progressive’s increase averages 35–50%, and its accident forgiveness program (available in most states) can shield your first incident entirely.

- One Speeding Ticket: Progressive often beats GEICO by $200–$400 annually for a single minor violation.

- DUI or SR-22/FR-44 Requirement: This is Progressive’s territory. GEICO frequently declines SR-22 filings or prices them so high that the quote becomes uncompetitive. Progressive writes these policies daily and keeps rates in the $2,800–$4,200 range depending on state.

- Young Drivers (Under 25): Progressive’s rates for drivers aged 18–24 are consistently 10–18% lower than GEICO’s, especially when the young driver has a clean record and enrolls in Snapshot.

If your driving abstract contains anything other than zeros, start your comparison shopping with Progressive. You will likely get a second quote from GEICO that confirms the gap.

Claims Experience and Customer Service Reality

Premium savings evaporate quickly if the claims process is a nightmare. The 2025 J.D. Power U.S. Auto Insurance Study and the NAIC Complaint Index paint a clear picture of what happens after an accident.

- J.D. Power Overall Satisfaction (2025): GEICO scored 874 out of 1,000. Progressive scored 862. Both rank above the industry average, but GEICO holds a measurable edge in claims satisfaction and policy communication.

- NAIC Complaint Index: GEICO’s complaint ratio sits at 0.75 (meaning it receives 25% fewer complaints than expected for a company its size). Progressive’s ratio is 1.05, slightly above the national median of 1.0.

- Mobile App and Digital Tools: Progressive’s app is frequently rated as more intuitive and feature-rich, especially for filing claims and uploading photos. GEICO’s app is highly functional but slightly less polished. Both offer 24/7 claims intake.

If claims handling is your top priority, GEICO has the statistical edge. If you value a frictionless digital experience above all else, Progressive’s technology stack wins.

Definitive Buyer’s Guide: Who Chooses Which in 2026

We have distilled hundreds of rate comparisons into clear buyer profiles. Find where you fit.

Choose GEICO If…

- Your driving record is spotless and your credit score is above 700.

- You are active military, a veteran, a federal employee, or an immediate family member of one.

- You insure two or more vehicles and want the deepest multi-car discount available.

- You prioritize a low-complaint, high-satisfaction claims experience.

- You want simple, no-telematics policies without monitoring.

Choose Progressive If…

- You have a ticket, accident, or DUI on your record within the last five years.

- You are under 25, or you are adding a driver under 25 to your policy.

- You drive fewer than 8,000 miles annually and can prove it through Snapshot.

- You need an SR-22 or FR-44 filing to reinstate your license.

- You drive for Uber, Lyft, DoorDash, or Instacart and need a rideshare endorsement.

The 15-Minute Rule That Saves You Real Money

No review, no expert opinion, and no brand loyalty replaces the raw math of binding a quote. GEICO and Progressive both offer online quoting engines that return a real, bindable price in under fifteen minutes. You should run them side-by-side on the same day, using identical coverage limits and deductibles, because rates shift weekly based on each carrier’s loss ratios and internal targets. A quote you pulled in March could be $300 different in April.

Do not leave money on the table because one company’s gecko or another’s spokesperson made you laugh. The cheapest policy for your exact risk profile is a math problem, and you now have the formula to solve it.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: GEICO and Progressive rate filings (2026), Quadrant Information Services, J.D. Power 2025 U.S. Auto Insurance Study, NAIC Complaint Index, state departments of insurance.