You are staring at two declaration pages. One from Progressive, one from Allstate. The premium numbers are separated by $500, and the coverage descriptions read like a foreign language. If you pick wrong, you either leave a massive discount on the table or—worse—buy a policy that crumbles the moment you file a claim. Progressive has built its empire on data, telematics, and a willingness to insure almost anyone. Allstate has staked its reputation on local agents, premium add-ons like accident forgiveness, and a vanishing deductible that rewards long-term loyalty. The gap between them is not just about price. It is a fundamental collision between two opposing philosophies of what car insurance should be. This guide pulls back the curtain on their 2026 rates, the fine print behind their most-hyped features, and the exact driver profiles each carrier serves best.

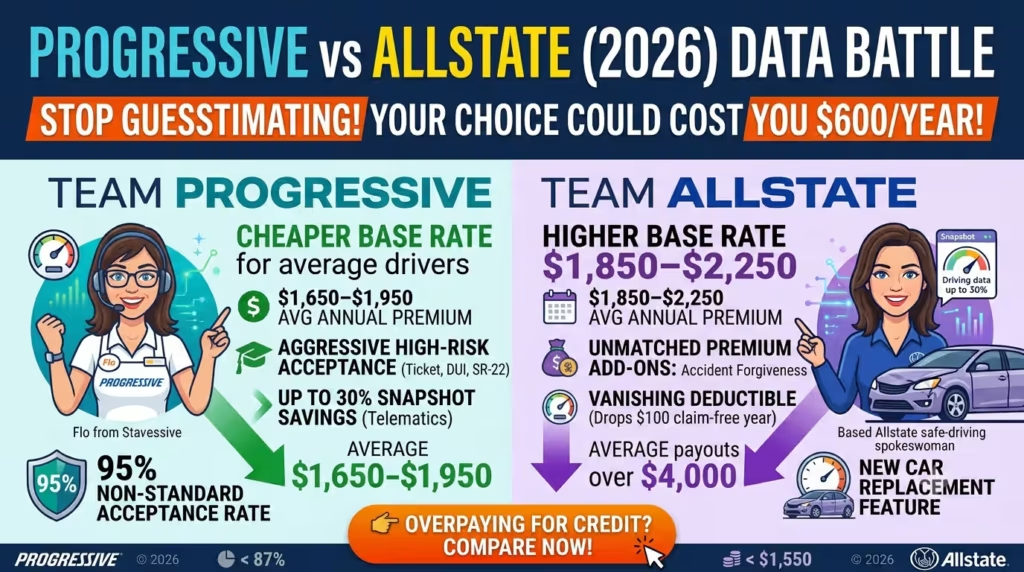

Quick Answer: For the average driver with a clean record, Progressive is 10–15% cheaper than Allstate, with full-coverage premiums averaging $1,650–$1,950 compared to Allstate’s $1,850–$2,250. Progressive also holds a commanding lead for high-risk drivers. Allstate wins only if you specifically value unique coverage add-ons—accident forgiveness, vanishing deductible, and new car replacement—and are willing to pay $300–$600 more per year to get them.

We dissect rates, discount mechanics, coverage features, claims satisfaction data, and the high-risk driver landscape to give you a decision framework that ends the guesswork.

Head-to-Head Premium Analysis for 2026

Using aggregated rate filings for a 40-year-old driver carrying full coverage (100/300/100 liability, comprehensive and collision with a $500 deductible) and driving 12,000 miles annually, the price gap between Progressive and Allstate is immediate and significant.

- Progressive Average Annual Premium: $1,650–$1,950

- Allstate Average Annual Premium: $1,850–$2,250

Progressive’s structural advantage comes from its advanced pricing models, which aggressively segment risk and reward safe drivers through telematics. Allstate’s higher base rates reflect the cost of its extensive agent network and the embedded value of its add-on features. For identical liability and physical damage limits, Progressive consistently undercuts Allstate by a margin that exceeds $300 annually across most states. The gap widens for drivers with violations and narrows only slightly for those insuring brand-new vehicles, where Allstate’s new car replacement coverage may offset some of the premium difference in perceived value.

Coverage Features: A Weaponized Comparison

Price alone is meaningless without understanding what each policy actually delivers. Both carriers offer standard coverage options—liability, collision, comprehensive, medical payments, uninsured motorist—but their standout features reveal who they truly serve.

Progressive Standout Features

- Name Your Price Tool: You input a budget, and Progressive builds a policy that fits it. This tool is particularly powerful for drivers who need to hit a specific monthly payment without sacrificing essential protection.

- Snapshot Telematics: Up to 30% discount for safe driving monitored through a mobile app or plug-in device. Progressive was the first major carrier to offer usage-based insurance at scale, and its discount is still among the most aggressive in the industry.

- Rideshare Endorsement: Covers the gap between personal insurance and Uber/Lyft coverage during Periods 1 and 2. Available in most states, and competitively priced at $15–$30 per month.

- Pet Injury Coverage: Up to $1,000 in veterinary bills if your dog or cat is injured in a covered accident. A niche but emotionally powerful benefit for pet owners.

- Custom Parts and Equipment Coverage: Protects aftermarket modifications like custom wheels, stereo systems, and performance upgrades.

- Loan/Lease Payoff (Gap Insurance): Pays the difference between your car’s actual cash value and the remaining loan balance if your vehicle is totaled.

Allstate Standout Features

- Accident Forgiveness: Available as a paid add-on or earned after five years claim-free. Your first at-fault accident does not increase your premium. Progressive offers similar forgiveness in limited states, but Allstate packages it as a core upgrade.

- Vanishing Deductible: Your collision deductible drops by $100 for every year you drive without an accident, potentially reaching zero. No other major carrier offers this exact structure.

- New Car Replacement: If your vehicle is totaled within its first two model years, Allstate pays to replace it with a brand-new model—not just the depreciated actual cash value.

- Drivewise Telematics: Up to 25% discount for safe driving. While slightly less generous than Snapshot, Drivewise offers an easy-to-use app experience.

- Household Liability Coverage: Extends certain liability protections to family members living in your household who may not be named on the policy.

The strategic fork is clear: Progressive invests heavily in pricing technology and flexible coverage for modern driving behaviors. Allstate invests in loyalty mechanics and premium replacement value for high-value assets. Choose based on what you actually need, not what sounds impressive in a commercial.

High-Risk Drivers: The Decisive Progressive Advantage

If your motor vehicle record contains a speeding ticket, an at-fault accident, a DUI, or a lapse in coverage, the choice between these two carriers collapses into a single data point. Progressive actively courts non-standard risks. Allstate frequently declines them or prices them so high that the quote becomes irrelevant.

- One speeding ticket: Progressive’s increase averages 15–25%, while Allstate’s can reach 30–40%.

- One at-fault accident: Progressive’s premium rises 35–50%. Allstate’s can spike 50–70%, and accident forgiveness must be purchased before the incident occurs to apply.

- DUI or SR-22 requirement: Progressive writes these policies routinely and maintains a dedicated high-risk underwriting division. Allstate may refer you to a partner carrier or decline coverage outright.

- Poor credit score: Progressive’s pricing models penalize low credit less harshly in many states, giving it a clear edge for drivers rebuilding their credit.

If your driving abstract contains anything other than zeros, Progressive will almost certainly be both the cheaper and the more accessible option. Allstate’s risk appetite narrows sharply outside of preferred-tier business.

Safe Drivers: A Closer Fight

For drivers with spotless records and excellent credit, the competition tightens. Progressive’s Snapshot program offers a potential 30% discount, which can swing a policy $400–$600 below Allstate’s best rate. Allstate counters with its vanishing deductible, which reduces out-of-pocket costs over time in a way that Snapshot cannot replicate. The smart play for safe drivers is to run both numbers and project five-year costs. If you plan to stay with the same company, Allstate’s vanishing deductible plus new car replacement could tip the scale. If you want the lowest premium today and are willing to switch carriers at renewal, Progressive’s telematics edge typically wins.

Customer Service and Claims: Where Agents Meet Algorithms

Both carriers perform above the industry average, but their service delivery models could not be more different.

- J.D. Power Overall Satisfaction (2025): Allstate scored 868, edging out Progressive’s 862. Both scores land above the industry average and are too close to call a definitive winner.

- NAIC Complaint Index: Allstate holds a slightly better ratio at 0.95 compared to Progressive’s 1.05. Both hover near the industry baseline of 1.0, indicating average complaint volumes.

- Claims Experience: Progressive’s fully digital claims process produces faster average payout times, especially for straightforward collisions. Allstate’s agent-centric model offers more personalized guidance through complex liability disputes.

- Agent Access: Allstate maintains a large network of exclusive agents you can visit in person. Progressive operates primarily through phone, app, and website, with independent agents available in some regions.

If you want a human being to sit across a desk from you and explain your policy, Allstate has the edge. If you prefer to manage everything from your phone and prioritize speed over hand-holding, Progressive’s digital infrastructure is superior.

Definitive Buyer’s Guide: Who Chooses Which in 2026

We have mapped hundreds of quotes and coverage scenarios to these clear profiles. Find your fit.

Choose Progressive If…

- You have a ticket, accident, DUI, or SR-22 filing on your record.

- You drive for Uber, Lyft, DoorDash, or Instacart and need a rideshare endorsement.

- You are comfortable with telematics and want the deepest possible safe-driving discount.

- You want the lowest annual premium for identical coverage limits, period.

- You prefer managing your policy entirely through a mobile app without agent interaction.

Choose Allstate If…

- You drive a brand-new vehicle and want guaranteed new car replacement.

- You plan to stay with the same carrier for five or more years and want to accumulate vanishing deductible credits.

- You value having a local agent you can visit in person.

- You are willing to pay a premium for accident forgiveness and premium customer service.

The 10-Minute Rule That Protects Your Wallet

Neither brand loyalty nor a single comparison article should dictate your choice. Progressive and Allstate both allow you to bind a real quote online in under ten minutes. Run them side-by-side with identical liability limits and deductibles. Compare the premium. Read the fine print on accident forgiveness and vanishing deductibles if you lean Allstate. Check the Snapshot enrollment discount if you lean Progressive. The carrier that wins is the one that puts the lowest dollar figure on the coverage you actually need.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: Progressive and Allstate rate filings (2026), Quadrant Information Services, J.D. Power 2025 U.S. Auto Insurance Study, NAIC Complaint Index, company coverage documentation and underwriting guidelines.