The letter arrives. You open it expecting a check to fix your car or cover your medical bills. Instead, one sentence hits you like a freight train: “We regret to inform you that your claim has been denied.” Panic sets in. Then anger. You did everything right—paid premiums on time, reported the accident immediately—and now your insurer is walking away. In that moment, most drivers assume the fight is over. It is not. Insurance claim denials are reversed every single day, often without a lawyer, because policyholders understand how to push back.

Quick Answer: A denial letter is not a final verdict. You have the right to an internal appeal, a review by your state’s Department of Insurance, and—if the insurer acted in bad faith—a lawsuit that can yield damages beyond the original claim. The most common reasons for denial (missed deadlines, policy exclusions, alleged misrepresentation) are frequently overturned when you submit the correct documentation, cite the right policy language, and escalate the dispute methodically. Start your appeal within 30 days to preserve every legal right.

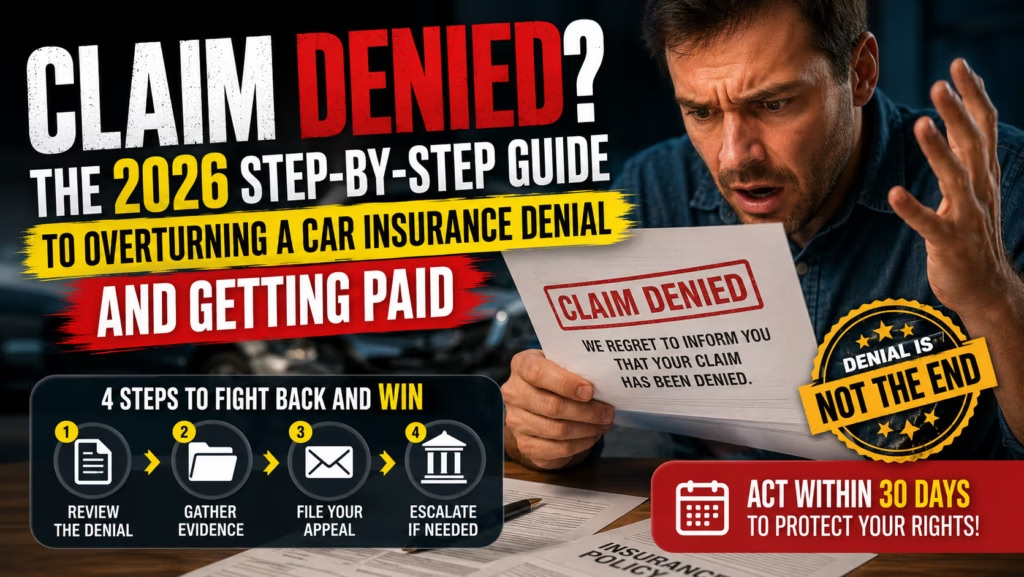

Here is exactly why your claim was denied, how to read the denial letter like an adjuster, the four-step escalation process that works, and the critical mistake that can permanently kill your chances of recovery.

The Real Reasons Insurance Companies Deny Claims

Insurers are for-profit corporations, and denial is often a first offer—not a final answer. Understanding the precise grounds they cite lets you dismantle their reasoning. These are the eight most common denial triggers, along with the counterarguments that defeat them:

- Lapsed policy / non-payment: The carrier says your coverage was not active at the time of loss. If you have bank records or a payment confirmation number proving the premium cleared before the accident date, this denial collapses immediately.

- Policy exclusion: The accident type is listed as not covered—commercial use of a personal vehicle, racing, intentional acts, wear and tear. Many exclusions have exceptions. A rideshare exclusion, for example, may not apply if you were not logged into the app at the moment of the crash. Demand the exact policy section and read every word.

- Material misrepresentation: The insurer claims you lied or omitted something on your application—annual mileage, household drivers, vehicle modifications. Under state law, the insurer must prove the misrepresentation was deliberate and that they would not have issued the policy had they known the truth. A simple error (guessing 12,000 miles instead of 14,500) rarely qualifies.

- Late notice: You did not report the accident within the timeframe required by the policy (often 30 days). Many states require the insurer to prove they were actually harmed by the delay. If you were hospitalized, language barriers existed, or the damage was not initially apparent, the denial can be reversed on appeal.

- No valid license or excluded driver: The person behind the wheel was not listed on the policy or lacked a valid license. If the driver was a permissive user (you gave them the keys) and lived outside your household, standard policies often still cover the loss.

- Lack of cooperation: You missed an adjuster call or did not submit a form. Cooperation is a condition of coverage, but insurers must show they made reasonable attempts to reach you and that your non-response was prejudicial. A single missed call is not enough.

- Disputed liability: The carrier believes you were at fault and denies first-party or third-party benefits accordingly. Police reports, dashcam footage, and independent witness statements can flip this determination.

- Coverage limits exhausted: The insurer paid up to the policy limit and closed the rest. While this is technically a partial denial, it can be challenged if the insurer failed to adequately defend you and caused the excess judgment.

How to Read a Denial Letter Like a Claims Attorney

Every denial letter contains specific language that dictates your next move. Do not skim it. Identify these three elements immediately:

- The exact policy provision cited. It must reference a section number or specific exclusion clause. If the letter is vague (“your policy does not cover this type of damage”), demand a written clarification with the precise language. Under the Unfair Claims Settlement Practices Acts in nearly every state, you have the right to a clear explanation.

- The deadline to appeal. Most policies give you 30 to 60 days to request an internal review. If you miss this window, you may forfeit the right to challenge the denial entirely. Mark the calendar and treat this date like a court deadline.

- The contact information for the appeals unit or claims supervisor. This is the person who can overturn a line-level adjuster’s decision. Bypass the call center and send a written appeal directly to the named individual.

The Four-Step Appeal Process That Reverses Denials

Move through these stages in order. Each step generates a paper trail that strengthens your position for the next level of escalation.

Step 1: File a Formal Internal Appeal with Evidence

Write a concise, professional letter (certified mail, return receipt requested) that states:

- Your claim number, date of loss, and the denial date.

- A clear sentence explaining why the denial is incorrect, referencing the policy language the insurer cited and your counter-evidence. Example: “You denied coverage under Exclusion 3.2 (business use), but I was driving to a personal dinner, as evidenced by the receipt and witness statement attached.”

- All supporting documents: police report, photos, repair estimates, medical records, proof of premium payment, correspondence with the adjuster, and any voice recordings (where legally obtained).

- A request for a written response within 15 business days.

Step 2: Escalate to a Claims Supervisor and the Insurer’s Compliance Department

If the internal appeal is rejected or ignored, send the identical packet to the claims supervisor, the company’s complaint/compliance department, and the CEO’s office. A single letter to an executive’s office frequently triggers a file review by a senior analyst who is not emotionally attached to the initial denial. Include the line: “I am prepared to file a complaint with the state Department of Insurance if we cannot reach resolution within 10 days.”

Step 3: File a Complaint with Your State Department of Insurance (DOI)

Every state has a Department of Insurance that regulates carriers and investigates consumer complaints. Filing a complaint is free, takes approximately 20 minutes online, and is statistically effective: many carriers reverse borderline denials the moment a DOI investigator requests the claim file. Go to NAIC.org to find your state’s DOI portal. Attach your entire paper trail. The DOI will forward your complaint to the insurer and require a written response within a statutory timeframe—usually 15 to 30 days. The process also generates a public record, which insurers dislike.

Step 4: Consult a Bad Faith Insurance Attorney

If your claim is worth over $5,000 and the denial appears unreasonable, an attorney who specializes in bad faith insurance litigation can force payment—and potentially recover damages beyond the original claim, including legal fees, emotional distress, and punitive damages. Many work on contingency, taking 30–40% of the final recovery. The initial consultation is nearly always free. A single demand letter on law firm letterhead sometimes resolves the dispute within a week.

When the Denial Is Your Fault: Fixing Honest Mistakes

If you genuinely made an error on your application—forgot to list a teenage driver, underestimated annual mileage—do not panic. Many states follow the “material misrepresentation” standard, which requires the insurer to prove the error was intentional and would have changed the policy issuance. If the mistake was minor, you can often offer to pay the additional premium retroactively and have the claim reinstated. Call the insurer’s underwriting department, explain the oversight, and ask if they will accept a policy correction. Proactive honesty frequently saves the claim and your coverage.

Real-World Overturn: A Denial That Should Never Have Happened

After a deer collision, a State Farm policyholder received a denial stating the comprehensive deductible was $1,000 and the repair estimate was only $900, so “no coverage applied.” The policy language contained no minimum claim threshold—the insurer simply owed $0 after deductible subtraction but was still obligated to open and document the claim without labeling it denied. The policyholder appealed with the policy page, and the insurer corrected the record, removing the denial from the claims history. This prevented a future rate increase that a denied claim marker would have triggered. The lesson: read the policy, not just the adjuster’s summary.

Protect Yourself from Future Denials Starting Today

The best appeal is the one you never have to file. Minimize your denial risk with these concrete habits:

- Read your policy’s exclusions page today—especially language around business use, unlisted drivers, and intentional acts.

- Update your carrier whenever a licensed driver moves into your household, your annual mileage changes significantly, or you modify your vehicle.

- Report every accident immediately, even single-vehicle incidents where damage seems minor. Delayed reporting is one of the leading causes of denial.

- Keep your premium payments on autopay and maintain proof of payment records.

- Take date-stamped photos of your car at the start of each policy term to document pre-existing damage.

A denial is a negotiation, not a funeral. Gather your evidence, write the appeal, and escalate relentlessly. The system is designed to be navigated, and the most persistent policyholders walk away with checks the insurance company initially refused to write.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: National Association of Insurance Commissioners (NAIC) Unfair Claims Practices Act, Insurance Information Institute (III) Consumer Claims Guide, state Department of Insurance complaint portals, American Bar Association Section of Insurance Litigation, Federal Trade Commission report on claims dispute resolution.