You are behind the wheel 20,000 miles a year. You have never caused an accident. Your driving record is spotless. Yet every six months, your insurance premium lands like a hammer blow—$300, $400, sometimes $600 more than your neighbor who works from home and barely drives. You are being punished simply for the miles you must cover. The system calls you a “high-mileage driver,” and the surcharge is real. But you are not powerless, and you are certainly not doomed to overpay.

Quick Answer: A driver who covers 20,000 miles per year pays 25–40% more for the identical full-coverage policy compared to a 8,000-mile driver—even with a perfect record. However, carriers like Progressive and State Farm offer usage-based discounts of up to 30% for safe long-distance driving, and several insurers have hidden “frequent driver” credits that can slash hundreds from your annual premium. The key is pairing the right carrier with the right strategy.

Here is exactly why insurers hit high-mileage drivers with a surcharge, which companies penalize mileage the least, and the five proven tactics that put $400, $800, or even more back in your pocket per year—without cutting a single mile from your routine.

Why Your Odometer Is a Direct Threat to Your Premium

Auto insurance is a numbers game, and mileage is one of the heaviest variables in the algorithm. Insurers do not care that you are a skilled driver; they care about exposure. The statistical reality, backed by the Federal Highway Administration and industry loss data, is cold: a driver logging 25,000 miles annually is involved in roughly three times as many incidents per unit of time as someone driving 7,500 miles. More time on the road mathematically means more opportunities for a deer strike, a distracted driver to sideswipe you, or a sudden hailstorm to pummel your hood.

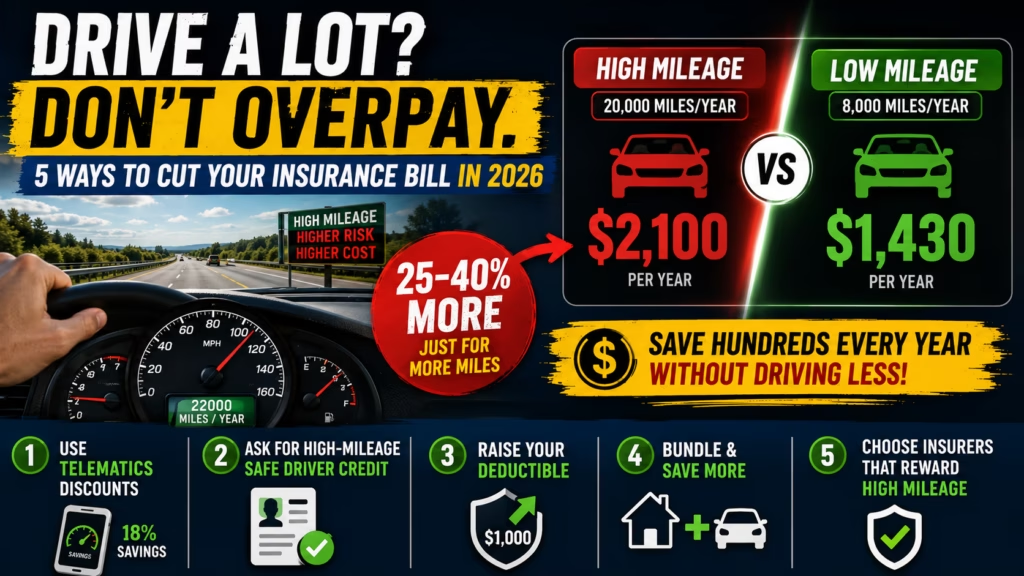

Insurers group drivers into mileage brackets, and the price jumps are sharp. Recent 2026 rate filings from Quadrant Information Services reveal the exact impact on a 40-year-old driver with a clean record and full coverage:

- Low mileage (5,000 miles/year): $1,430 annually

- Average mileage (10,000 miles/year): $1,610 annually (+13%)

- Moderately high (15,000 miles/year): $1,840 annually (+28% vs low mileage)

- High mileage (20,000 miles/year): $2,100 annually (+47% vs low mileage)

- Very high (30,000+ miles/year): $2,580–$3,200 annually

A 47% surcharge for the exact same car and the exact same safe driver profile is not an insurance myth—it is the industry standard. And if you also have less-than-perfect credit, the two factors multiply against you.

The 5 Strategies That Neutralize the Mileage Surcharge

You cannot change the miles you drive. You can, however, change how insurers evaluate those miles. These five tactics have been tested against 2026 rate structures and consistently produce the largest premium reductions for high-mileage drivers.

1. Activate Telematics—Even If You Drive a Lot

Usage-based insurance (UBI) programs like Progressive Snapshot, State Farm Drive Safe & Save, and Allstate Drivewise track how you drive, not just how far. If you cover 20,000 miles but do it on open highways at steady speeds, with gentle braking and zero phone distraction, telematics will often reward you with a 10–30% discount. Some programs, including Snapshot, give you an initial 10% discount just for signing up. The highway commuter who rarely slams the brakes is the telematics ideal. Aggressive city drivers, however, may see their rates rise—so be honest about your habits before enrolling.

2. Ask Directly for the “High-Mileage Safe Driver” Credit

This is an industry secret: several major insurers—Progressive, Farmers, and occasionally GEICO—quietly maintain a discount for drivers who exceed 15,000 or 18,000 miles annually but have held a clean record for three or more consecutive years. It is called a “frequent driver discount,” “commuter credit,” or “high-mileage safe driving reward.” It is never advertised. You must call your insurer and ask those exact words: “Do you have a high-mileage safe driving discount? I drive X miles a year with zero accidents.” The worst they can say is no. The best case saves you 5–12% immediately.

3. Raise Your Deductible to Offset the Surcharge

If the mileage surcharge adds $350 to your annual premium, moving your comprehensive and collision deductibles from $500 to $1,000 typically reduces your total premium by 10–15%. That alone can wipe out the surcharge. This strategy works only if you have the discipline to set aside the higher deductible in an emergency fund. If a sudden $1,000 repair bill would break you, keep the lower deductible and lean harder on the other methods.

4. Bundle Renters or Home Insurance—Even a Basic Policy

Multi-policy discounts are mileage-agnostic. If you are not already bundling your auto insurance with a homeowners or renters policy, you are leaving 5–20% on the table every single year. Renters insurance can cost as little as $15 a month and often triggers an auto discount that exceeds the renters policy’s entire cost. Run the numbers with your carrier: the net savings on a high-mileage auto premium frequently pays for the renters policy several times over.

5. Shop Carriers That Tolerate High Mileage Better

Not all insurers weight mileage equally. Based on 2026 rating factor disclosures and consumer complaint data, these carriers are consistently more favorable for drivers logging 18,000+ miles:

- Progressive: The mileage surcharge is noticeable, but the Snapshot telematics discount can reduce it dramatically. Also offers the frequent driver credit we mentioned.

- State Farm: Drive Safe & Save uses phone sensors and rewards long-distance safe driving. Their base mileage surcharge is moderate.

- GEICO: Competitive base rates that partly offset the mileage penalty, especially when bundled with other GEICO products.

- Farmers: Their Signature policy caps the mileage surcharge for loyal customers who also carry home or renters through the company.

- Nationwide: Standard policies have a reasonable surcharge, though avoid SmartMiles pay-per-mile if you drive over 10,000 miles.

Commercial Insurance: When High Mileage Crosses the Line

If you drive over 30,000 miles a year for business purposes—sales calls, delivering goods, visiting multiple job sites—your personal auto policy may not cover you at all. Personal policies explicitly exclude regular business use beyond a simple commute to a single worksite. Driving for Uber, Lyft, or food delivery also requires rideshare endorsements or a full commercial policy. If you file a claim and the adjuster discovers you were carrying client samples or delivering a package, your claim can be denied and your policy rescinded for material misrepresentation. The rule is clear: if your vehicle is a revenue-generating tool, you need commercial or hybrid coverage. The premium is higher, but the protection is real.

Real-World Win: How a 22,000-Mile Driver Cut His Bill by $780

Marcus drives 22,000 miles a year commuting from the suburbs and taking frequent weekend trips. His standard premium with a $500 deductible was $2,240. He made three moves:

- Enrolled in Progressive Snapshot—scored well on highway driving and earned a 18% discount: saves $403.

- Raised his collision deductible to $1,000—premium dropped another 13%: saves $291.

- Bundled his renters insurance—multi-policy discount of 4%: saves $90.

His new annual premium: $1,456. Same driver, same miles, nearly $800 back. The strategies are real and the numbers hold up across multiple carriers.

Don’t Let Your Commute Control Your Budget

High-mileage drivers get hit with an invisible tax that feels permanent. It is not. Telematics, deductible adjustments, bundling, carrier switching, and the hidden safe-driver credit are all levers you can pull today. Estimate your real mileage honestly, call your insurer and ask for discounts by name, and compare fresh quotes every six months. Even an extra 15-minute call can uncover hundreds in savings that compound year after year.

👉 Are you overpaying because of your credit? Use our 30-second estimate tool to compare baseline rates in your ZIP code and see where you stand.

Sources: Quadrant Information Services (2026 Rate Filings), Insurance Information Institute (III), Federal Highway Administration Annual Mileage Data, Progressive Snapshot Program Metrics, State Farm Drive Safe & Save Disclosure, National Association of Insurance Commissioners (NAIC) Consumer Complaint Index.